The 1980s rhythm was quite different in the way it dealt with money. A lot of households had tight finances, the prices were increasing, and there were fewer conveniences in the household, but still, daily life was heading somewhere with the feeling of balance. In the absence of applications or use of instant shops, individuals would simply tend to conduct business according to the habits that were common in the day. These habits were hardly presented as clever financial decisions, but they informally determined the manner in which money was managed. Regarding basic domestic decisions to considerate spending habits, these became a source of stability that could not be so apparent at the time. In retrospect, it is easier to observe how minor, regular behavior could help maintain financial fitness in a manner that is still familiar nowadays.

Using cash in everyday spending

Groceries and errands were usually done using cash. The physical transfer of money might have made it more real for people to spend; they could remain conscious of the boundaries without necessarily tracking their spending or calculating every transaction.

Repairing things rather than throwing them away

Wastes like broken items were usually repaired instead of being disposed of. Such an activity might have promoted patience and simple problem-solving, as well as straining the utility of domestic goods and decelerating unwarranted expenditures.

Wearing clothes till they wore out

There was no seasonal wear of clothes; they were worn over the years. Care and mending were common activities in families and could have lowered impulse buying and promoted the value of what was already possessed.

Planning shopping around sales

Most purchases were directed by weekly advertisements and seasonal bargains. Waiting until we could sell would have benefited the households by enabling them to purchase necessities at reduced prices, though this would have required additional time and effort in terms of planning ahead.

Driving cars for as long as possible

Automobiles were maintained till no longer economical. This would have minimized the number of regular payments and promoted routine maintenance so that a family could get more out of such a large purchase.

Sharing things within the home

There was the sharing of books, tools, and appliances. The practice could have minimized cases of buying the same item twice and also fostered collaboration, particularly in households where space and budget were highly considered.

Growing small home gardens

There were families that cultivated vegetables or herbs. Even the small gardens can contribute to reducing the grocery costs marginally, as well as to the consumption of local food and the sense of closeness to food suppliers.

Saving change and small amounts

Loose change would be stored in envelopes and jars. Emergency cushions might have been accumulated with these small savings habits, even though the amounts seemed inconsequential at the time.

Frequent credit use is to be avoided

There were credit cards, and they were not necessarily much utilized. Restricted usage could have prevented families from getting into long-term debt and trying to purchase items that better fit within existing funds.

Sharing objects with the younger siblings

Clothes and school supplies were regularly reused. Such a habit could have lowered the total expenditure as well as strengthened the perception that the objects could still possess some value even after their initial owner.

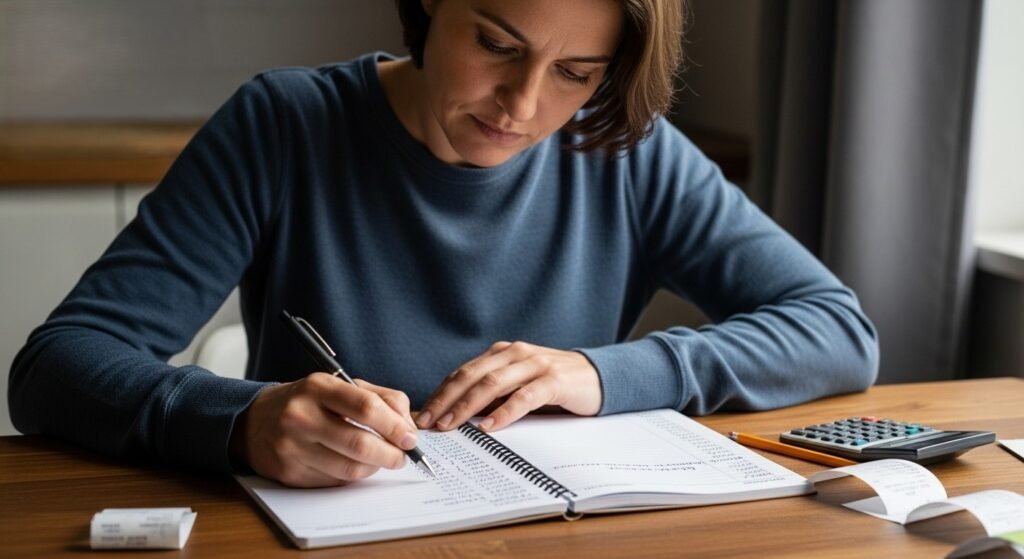

Simple pen and paper budgeting

Budgets were presented in written form. This simple method can have brought finances closer and simpler to grasp, despite the lack of intricate tools and more detailed classifications.

Choosing practical gifts

Gifts were usually utilitarian in nature and not trendy. Such an attitude might have relieved the need to spend excessively and still left consideration and compassion to drive special events.

Being patient with big purchases

Big buys were normally postponed and deliberated. Delayed purchases could have also enabled families to rethink need, timing, and cost and make decisions that would be more comfortable in the long run.